The emergence of insurtech in recent years has helped insurance companies to improve their customers’ experience, develop new products, lower costs and enhance underwriting and actuarial processes. But challenges around data privacy and equality of access need to be addressed.

The basic idea of insurance is based on risk transfer and has been around, in some form, for thousands of years. For example, Chinese merchants travelling through treacherous rivers over two thousand years ago would spread their goods across many vessels to avoid losing everything if a single vessel were to capsize. The use of public storehouse granaries for the purpose of communal protection in the event of a famine is another example.

Modern-day insurance can be traced back to events such as the Great Fire of London in 1666. This prompted the development of property insurance, the establishment of Edward Lloyd’s London coffee shop (which became a central place for marine insurance to develop and eventually the famous Lloyd’s of London insurance market) and the founding of the Amicable Society for a Perpetual Assurance Office in 1706 and the Equitable Life Assurance Society in 1762. These societies pioneered the use of age-based analysis for calculating the premiums for life insurance policies.

Fast forward to today and the world is clearly a very different place. New technologies are permeating almost every aspect of our daily lives. This has led to the world’s largest companies now being dominated by technology companies.

Despite the rapid advancement of technology in many sectors, insurance has – until recently – been described as a laggard in the adoption of innovative technology solutions. Mario Greco, the former chief executive of the Italian Generali Group, has warned that unless the insurance industry moves to the forefront of technological change, it will disappear.

But competitive pressures, changing customer expectations and the rise of digitalisation and mobile use have prompted both traditional insurers and innovative start-up companies to embrace technology in recent years. This use of technology to drive innovation within insurance is known as insurtech.

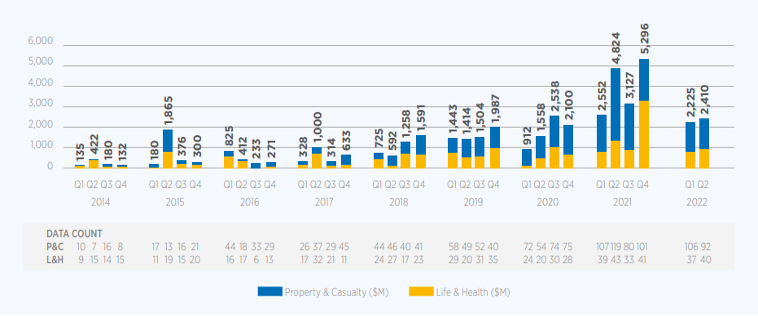

Now underway, the insurtech movement appears to be gaining significant momentum. This is highlighted by the funds flowing into the insurtech space (see Figure 1).

While it has been hit by the tech slowdown seen around the world in 2022 – caused by the economic uncertainties fuelled by inflation, supply chain issues and rising interest rates – total disclosed global insurtech funding rose from just under $1 billion in 2014 to almost $16 billion in 2021 (Gallagher Re Global InsurTech Report, 2022).

Figure 1: Quarterly insurtech funding volume, 2014-22

Source: Gallagher Re Global InsurTech Report for 2022 Q2

What new technologies is the insurance world adopting?

Artificial intelligence

Artificial intelligence (AI) is a catch-all term for a range of computer systems that can perform tasks that normally require human intelligence. These include activities such as visual perception, speech recognition and decision-making.

As a result of its actuarial nature, focused on predicting claims and hence setting appropriate premiums and reserves, insurance is a data-driven industry. Consequently, there are many potential applications for AI, including to:

- Enrich customer experience: for example, by providing initial quotations with minimal customer input. The AI-driven, California-based insurtech company Hippo provides such quotes and promises to do so within 60 seconds.

- Enhance claims handling: for example, to expedite claims, car insurance policy-holders can submit photographs, which are then run through image analysis such as that offered by US insurance giant, Allstate.

- Improve efficiencies: for example, the US insurtech firm Lemonade operates as a licensed insurance carrier and promises ‘instant everything’ (including quotations, switching policies and claims handling) through its use of AI-powered chatbots and 100% digital coverage.

- Reduce fraud: for example, the fully digital insurtech company Getsafe has identified 27 indicators of fraud and implemented automated checks in their system to monitor them continually.

Blockchain

Blockchain technology is a peer-to-peer data storage technology that aims to remove the need for intermediaries by providing a decentralised ledger and an irrefutable record of all historic transactions.

Blockchain is generally associated with cryptocurrencies, but its applications extend beyond this and show potential for insurance companies (Farrell, 2019).

One particularly interesting application of blockchain is the enabling of event-triggered smart contracts. In insurance, this typically involves four stages:

- Terms are agreed by the insurer and policy-holder to form a pre-defined contract. It is important that there are clear, objective and verifiable inputs that can dictate the terms of paying out a claim. This might include unambiguous events, such as a death recorded on a death registry or an official weather report in the case of crop insurance.

- The event occurs and is automatically recorded on the blockchain.

- The blockchain entry triggers the smart contract execution based on the contract’s pre-agreed terms.

- Settlement occurs in an instantaneous and efficient manner, via the blockchain, which also records the settlement.

Figure 2: Process for event-triggered smart contracts

There are many potential benefits of this blockchain-enabled smart contract. For example, the process is efficient and quickly executed, which lowers costs and reduces fraud via enhanced transparency. In addition, customer satisfaction is likely to improve.

Indeed, one of the big issues in insurance is that of poor consumer trust (Farrell, 2022). Policy-holders are often concerned that they won’t receive their expected pay-out should a claim arise (for example, due to an unknown clause).

Smart contracts have the potential to play a major role in re-establishing consumer trust by pre-determining the insurance pay-out and automatically executing the contract if certain pre-agreed conditions are met. This is extremely important for the industry, as the underlying premise of insurance is based on trust.

Are there any blockchain-enabled smart contracts already in use? One early pioneer is Etherisc – a decentralised insurance protocol that collectively builds insurance products using blockchain. This includes crop insurance that has automated pay-outs triggered by drought or flood events reported by government agencies; flight delay insurance triggered by recorded flight delays; and a hurricane protection product.

But blockchain also has limitations, which include changing regulation, security and privacy (many insurers are still concerned about adopting such a new technology due to cybersecurity concerns), initial capital costs and cultural adoption by its users.

Connected devices and wearables

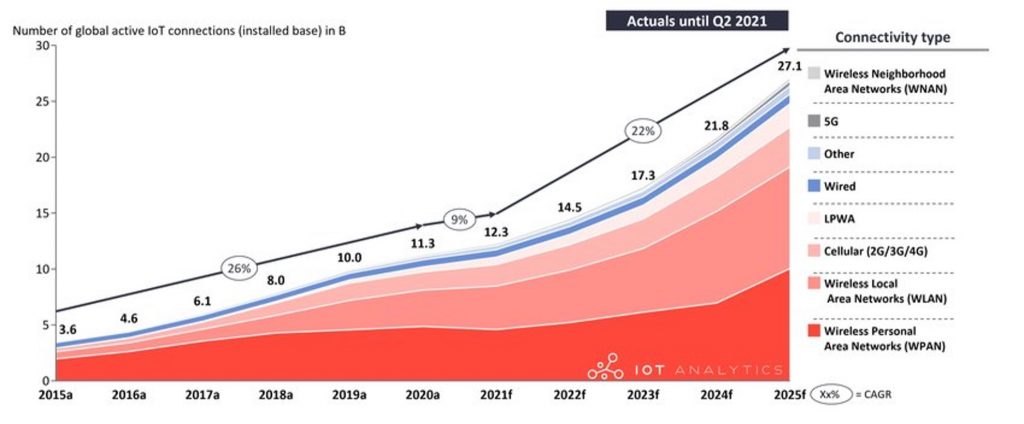

There has been an explosion of sensors and connected devices during the 21st century. IoT Analytics estimated there were over 13 billion connected Internet of Things (IoT) devices in 2021. These are physical objects with sensors that connect and exchange data over the internet or other communications networks (Gillis, 2021). This number is projected to grow to 27 billion by 2025.

Figure 3: Number of global active IoT connections

Source: Hasan, 2022

These devices – such as fitness trackers, smartphones, home assistants and smart watches – have enabled the constant collection of a significant amount of data. For the insurance industry, where data exist, opportunity abounds.

Connected home devices provide an opportunity and potential means for insurance companies to change the traditional insurer-insured relationship from protecting against damages to also helping to prevent them occurring in the first place. For example, a connected home device, provided by the insurer as part of a home policy, could detect a water leak and provide an instant alert to a smartphone.

Wearable fitness devices provide another exciting development for insurers. They provide a wide and growing range of possible data on behavioural and health metrics that can be advantageously used in insurance for benefits, such as product innovation, underwriting, product pricing and customer engagement (ProActuary, 2020). Many insurers, such as John Hancock, Oscar and UnitedHealthcare, have already embedded wearables into their products via innovative incentive schemes.

There are many avenues through which insurance is currently being disrupted by insurtech. These are just some examples, and we haven’t even mentioned technologies such as telematics and drones and other new emerging technologies, including autonomous vehicles and quantum computing.

Drones, for example, can help property insurers with risk assessment, damage monitoring and claims analysis. Further, the inevitable proliferation of autonomous vehicles will shift the risk and insurer liability from reckless driving by humans to risks such as malfunctioning software and cyber security.

What are the challenges ahead?

Insurtech is changing the insurance landscape in many positive ways. There are, of course, still many hurdles and challenges to overcome as new technologies are embedded into insurance companies.

Some of the big future challenges include privacy concerns from policy-holders sharing certain personal data (for example, from wearable devices). In particular, it will be important to ensure the fair treatment of individuals when selecting and using data, such as more advanced and accurate pricing algorithms that could make certain individuals uninsurable. General worries about the ethical use of big data also feed into the insurtech industry.

In summary, while there are challenges to overcome, it appears that the insurance industry is now entering a new era full of opportunities. Insurtech holds potential not only to transform but also to improve many aspects of the insurance chain. These changes can benefit both policy-holders and insurance companies.

Where can I find out more?

- Can insurtech rescue insurance? Mark Farrell on the role of technology in the insurance industry.

- Gallagher Re Global InsurTech Report for 2022 Q2: The latest quarterly insurtech report from global reinsurance firm, Gallagher Re.

- Insurtech UK: The trade association for the community of insurtech start-ups in the UK.

Who are experts on this question?

- David Lee Kuo Chuen, Singapore University of Social Sciences (SUSS)

- Liz McFall, University of Edinburgh

- Sabine VanderLinden, Honorary Senior Visiting Fellow at Bayes Business School